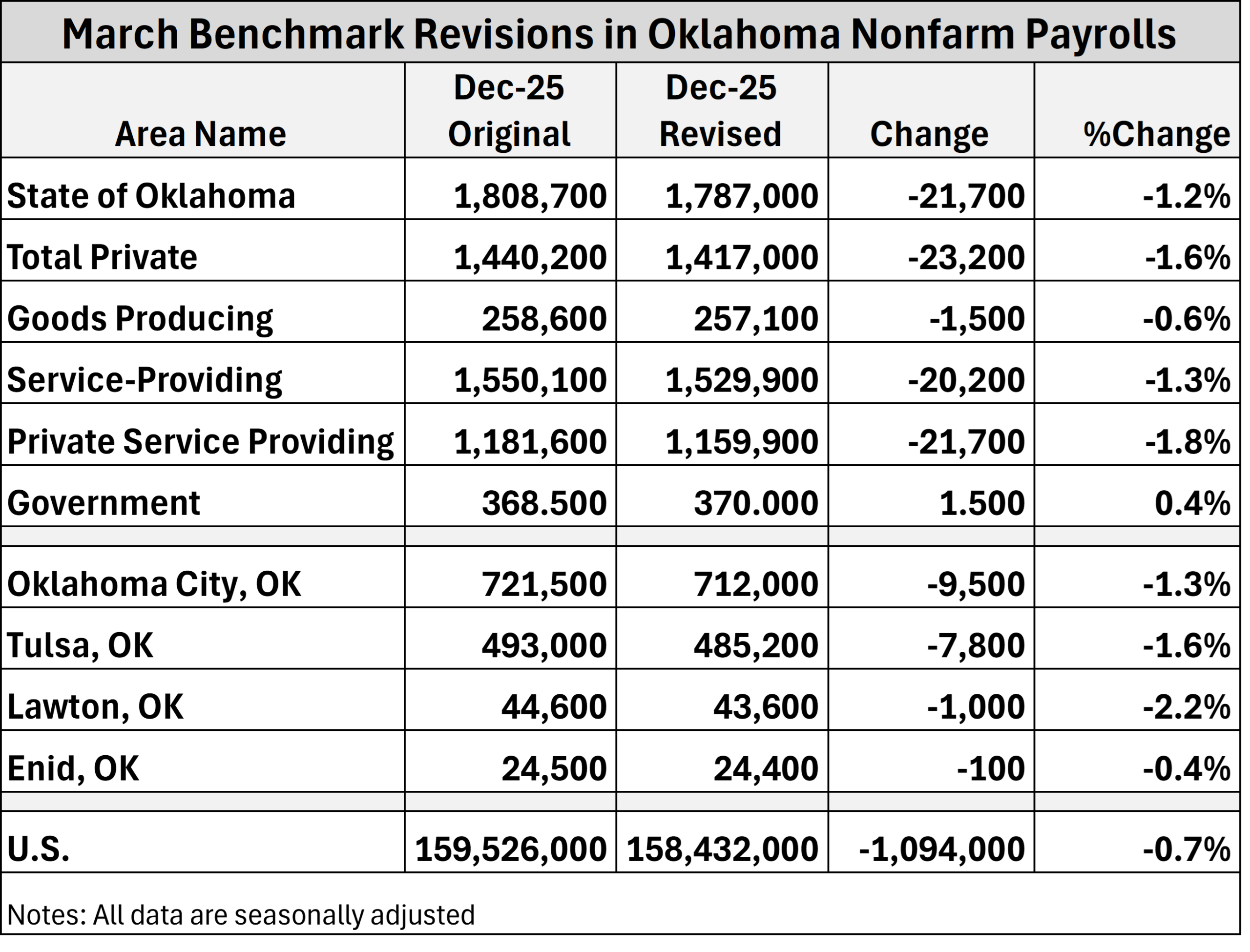

I haven't seen much discussion about the downward revisions to Oklahoma job data released earlier this month. We knew some weakness was coming, but the…

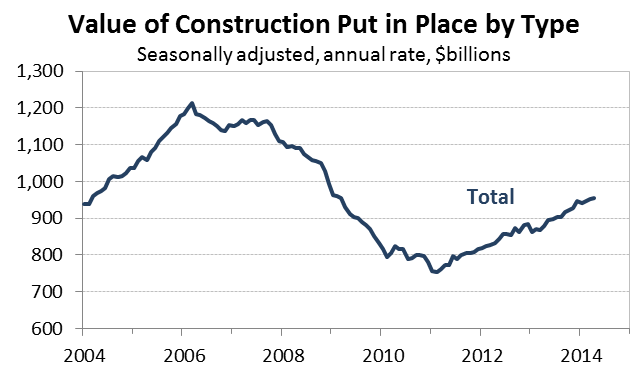

Pic-of-the-Week: Little Rebound in Construction Outside Residential (06/09/2014)

Residential construction rebound remains strong, but few other sectors showing gains – The recession took a deep toll on U.S. construction activity. Total activity declined by more than one-third from a $1.2 trillion annual pace to just $750 billion. The rebound began in early 2011 and has been steady, though far from spectacular. The pace of growth is much slower than the boom years prior to the recession, and activity has recovered less than half of the ground lost in the downturn.Â

So, what is doing well, and what isn’t?

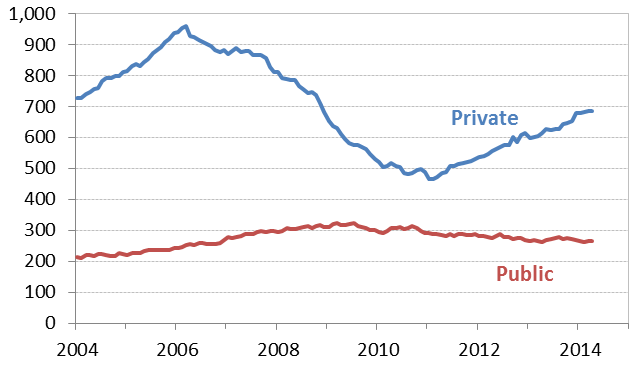

First, private activity is growing while public sector spending on construction continues to fall. Private sector construction is actually up 40% since the bottom. Public sector spending is down more than 10% from its 2009 peak.

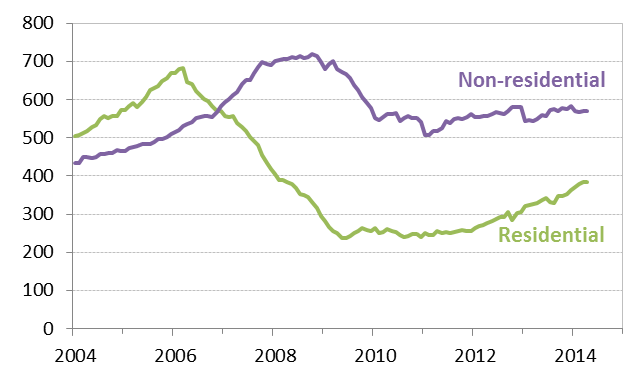

What is growing in the private sector? Mostly residential. It is up more than 60% since late 2011.

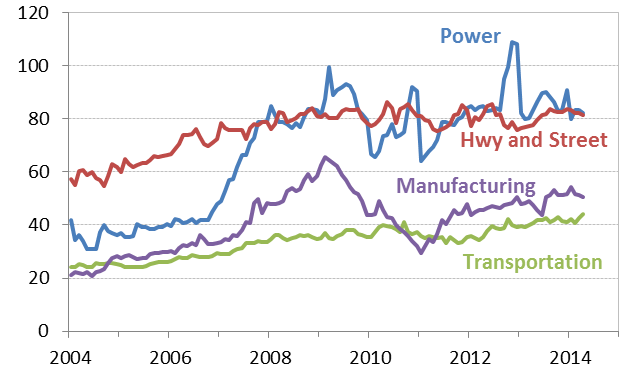

However, the very large and critical non-residential side of the private market  remains largely anemic. A few non-residential sectors are doing fairly well, though. The manufacturing sector has enjoyed a nice rebound, driven largely by energy-sensitive manufacturers seeking to take advantage of low natural gas prices. Transportation and highway/streets remain somewhat insensitive to economic conditions and remain in an uptrend. Finally, the power generation sector has remained at a high level of activity since the recession, but has shown little growth.

Most other major non-residential construction sectors, including office, health care, and education, remain either relatively flat or continue to fall.

Sign up to receive RegionTrack’s PIC OF THE WEEK!

[email_link]

[email_link]

Related Posts