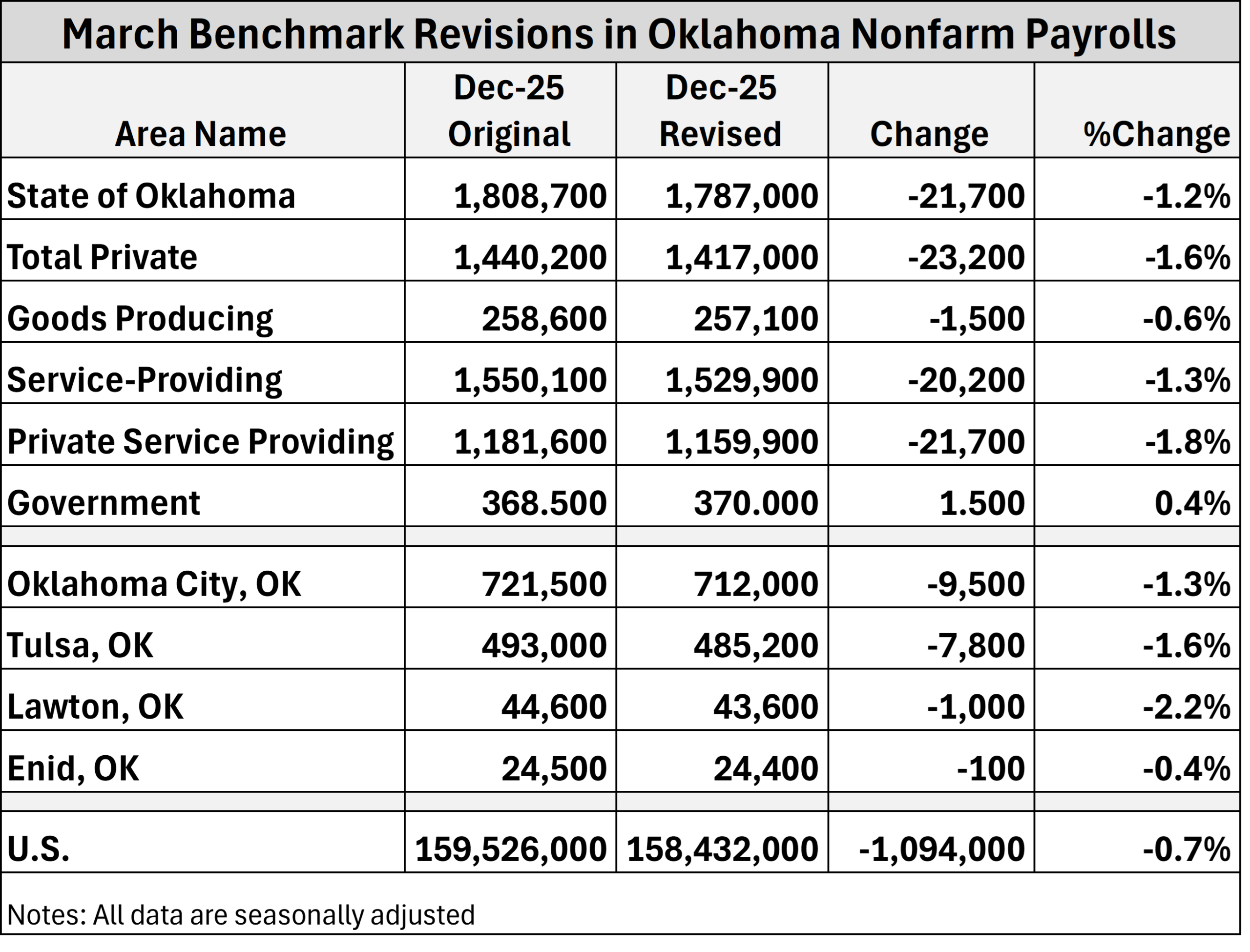

I haven't seen much discussion about the downward revisions to Oklahoma job data released earlier this month. We knew some weakness was coming, but the…

RegionTrack Report: Oklahoma Electricity Prices – Decomposition of Price Changes: 2020-2025

RegionTrack recently released a research report examining changes in electricity prices nationally and in Oklahoma from 2020 to 2025. The research evaluates the significance of the price increase relative to the nation and other states and explores the underlying causes of the price rise.

As it turns out, Oklahoma’s electricity cost story since 2020 has been more unusual than expected. The concern was that rising electricity costs might be acting as a meaningful constraint on the state economy. Our findings suggest that this has not broadly been the case, even though electricity prices clearly moved higher over the period.

A few points stand out:

- Oklahoma’s average electricity price rose 24.5% from 2020 to 2025, compared with 28.7% nationally. The increase in Oklahoma also almost exactly matched the rise in overall inflation over the period. In other words, electricity prices increased but not out of proportion to the broader inflation environment or relative to other states. By 2025, Oklahoma had returned to its position as the second-lowest electricity price state in the country.

- At the same time, electricity demand in Oklahoma grew 20.6%, versus 9.2% nationally. Nearly three-fourths of that increase occurred in the commercial sector, where sales rose 48%. That category includes data centers and other data-intensive commercial activity. Yet commercial electricity prices in Oklahoma rose only 16.0% over the period, compared with 29.7% for residential customers and 33.4% for industrial customers. Whether that pattern reflects differences in cost burdens across customer classes is an important question, but one that would require additional and deeper cost-of-service analysis.

- Utility-level outcomes differed sharply. OG&E’s average rates rose 25.3% from 2020 to 2025, close to the statewide average, while PSO’s rose 47.8%. Other providers also showed wide variation, ranging from 7.1% at OKEC and 13.8% at GRDA to 34.0% at Empire.

- Utility-level results matter not only because providers posted very different price increases, but also because a small number of utilities shape most of the statewide outcome. OG&E and PSO together account for roughly two-thirds of statewide electricity sales, and together with GRDA serve nearly three-fourths of end-use demand. At the same time, commercial load growth has been concentrated heavily within OG&E’s territory, where the commercial share of total sales rose from 34.2% in 2020 to 47.3% in 2025. As a result, Oklahoma’s recent electricity story is increasingly being shaped by territory-specific pricing, customer mix, and regulatory decisions rather than by statewide averages alone. Note that these utility-level price measures reflect average billed revenue per kilowatt-hour and are useful for identifying divergence in outcomes, but they do not by themselves establish the underlying cost-of-service relationships across customer classes or service territories.

- Winter Storm Uri clearly shaped the price path. Oklahoma began the period as the second-lowest electricity price state, moved as high as 14th after the post-storm surge, and returned to the second-lowest position by 2025. The immediate effect of the storm was a sharp rise in prices, followed in many cases by some reversal as rates adjusted over time. Even so, storm-related recovery charges will remain part of state electric bills for years to come.

- A comparison with Virginia is instructive. Virginia, the nation’s leading data center market, experienced even faster commercial load growth than Oklahoma. But Virginia’s electricity prices across major customer classes generally tracked or exceeded national trends, while Oklahoma’s commercial prices remained comparatively restrained. Rapid commercial expansion can raise concerns about infrastructure needs and cost allocation, but it does not by itself determine price outcomes.

The broader takeaway is that Oklahoma has so far managed to combine relatively restrained price growth with unusually strong commercial load growth. That is a favorable outcome, but it also raises a harder set of questions about infrastructure investment, rate design, and how future costs will be allocated across customer classes and service territories.

Report Link: https://www.regiontrack.com/www/wp-content/uploads/RegTrk-Oklahoma-Electricity-Price-Changes.pdf

Related Posts